In recent years, the banking industry has faced numerous crises that have shaken public trust and highlighted the importance of ethical considerations in banking. From the 2008 financial crisis to previous scandals involving money laundering, inappropriate bonuses, and fraudulent activities, it’s clear that the industry must address issues of conscience and values to restore confidence in the banking system. In this blog post, I’ll explore the concept of a “Crisis of Conscience” in the banking industry, its causes, and potential solutions. In a future post, I’ll also discuss the importance of ethical leadership and responsible practices in mitigating risks and promoting a healthier banking environment.

I am not a certified financial advisor but I have educated myself on personal finance and investment strategies. I am passionate about sharing my insights and empowering others to make informed decisions about their financial well-being. While seeking advice from a certified financial advisor is advisable for significant financial decisions, taking personal responsibility for our financial health and developing a basic understanding of economic principles is essential. I aim to use my knowledge to contribute to a financially literate society where individuals have the tools and knowledge to make informed decisions that positively impact their financial well-being. With all that said, let’s get into it.

The recent pandemic has caused widespread economic disruption worldwide, with many industries struggling to stay afloat and just starting to see the light at the end of the tunnel. One sector that’s been hit particularly hard is the banking industry. The United States, in particular, has been experiencing a banking crisis that has caused concerns for investors and regulators alike.

Crisis of Conscience?

The rise in interest rates is one cause of the current uncertainty in the banking sector. The Federal Reserve has the difficult job of reining in inflation without collapsing the economy. It is not an easy task after such extraordinary government intervention during the pandemic. In addition, with many businesses releasing employees and rising unemployment, we find ourselves in an environment that has put pressure on banks and financial institutions, which face losses on their loan portfolios, and bottom lines.

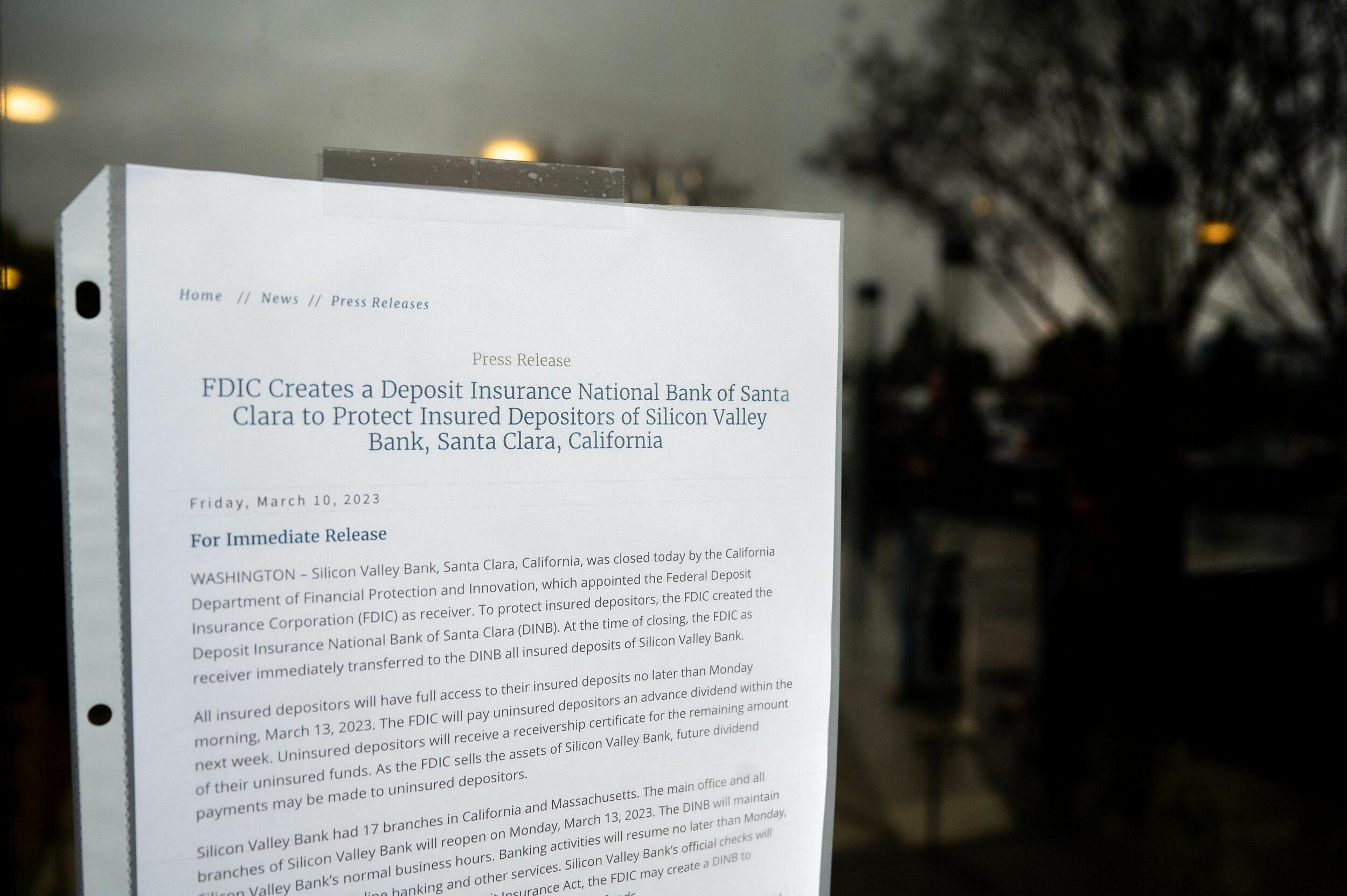

The current banking crisis has been exacerbated by higher interest rates and the collapse of Silicon Valley Bank (SVB). The banking crisis has not been limited to the USA, however. The Credit Suisse collapse, reportedly caused by divisive management, costly exposure to collapsed finance company Greensill Capital, a seedy money laundering case, and waning customer confidence, has, in the last few months, seen billions withdrawn from the bank. Even though UBS has agreed to Buy Credit Suisse for more than $3 Billion, this effort to prevent further erosion of confidence in the banking system isn’t appearing to be successful.

Many countries worldwide have been affected by these recent developments and experiencing similar economic uncertainty and market volatility issues.

There is still time to complete the three-pronged financial defensive posture! Cryptocurrency, Precious Metal stacking, and Traditional Assets!

What are the consequences of this current banking crisis?

The consequences of the bank crisis are far-reaching and potentially long-lasting. The current situation could lead to significant losses for banks and financial institutions, impacting their ability to lend money and provide financial services to their customers. These consequences could lead to a slowdown in economic activity, or what I believe could be a recession, and a further decline in consumer confidence in the overall system.

The system, as currently constructed, allows the Fed to manipulate the economy through its primary manipulation mechanism of rate adjustment. Their quick raising of rates and mismanagement of the current strategy has caused a problem in the system and the confidence of the banking industry as a whole. I’ve recently seen many online rants about banks being unable to provide their customers with cash when needed.

Banks only carry a little cash on hand for several reasons. Firstly, holding significant money is costly, requiring additional security measures and insurance to protect against theft or loss. Secondly, banks typically lend most of their deposits to borrowers, earning interest on those loans. This process means that they have limited funds available for cash reserves. Additionally, banks are required by law to maintain a certain level of reserves as a percentage of their deposits. These reserves are typically held as Federal Reserve deposits rather than in physical cash. Finally, cash transactions have become less common in today’s digital age, with many individuals and businesses using electronic payment methods instead. This new landscape has further reduced the need for banks to hold large amounts of physical cash.

Overall, while banks do need to maintain some cash on hand to meet customer demand and maintain liquidity, they typically do not carry significant amounts of money due to the costs and limitations involved. While this process and new money levels are the new normal for most banks, this practice has done damage to the consumers trust in banking institutions. This limitation with cash on hand has further played into the narrative that the banks are not doing well, and I believe more is needed to engender confidence in banking for customers and those speculating about the current environment. One of the primary issues with the banking industry is the narrative being painted by those in the know who feel we are heading for a recession, which could be worse than the 2008 recession.

What are the solutions?

To address the current bank crisis, several solutions are in play. These solutions include:

Government intervention

Many experts have called for government intervention to support banks and financial institutions. This intervention could take the form of direct financial support, such as loans, bailouts, or policy measures aimed at stimulating economic activity and propping up the failing banks.

Regulatory reform

Some experts have called for regulatory reform to address structural issues contributing to the many bank crises. These regulations could include improving transparency and accountability, strengthening risk management practices, and increasing capital requirements.

Innovation

Others have called for more significant innovation in the banking sector, mainly digital banking. These innovations could involve the development of new products and services better suited to the changing needs of consumers and businesses. However, one of the innovations that will face consumer resistance is the introduction of government-backed central bank digital currency (CBDC). CBDCs are digital currencies issued by central banks. Their value is linked to the issuing country’s official currency. Implementing the Fed CBDC poses an interesting mix of risks to the average banking consumer. (I have a CBDC post coming shortly)

Collaboration

Finally, some experts have called for greater collaboration between banks and financial institutions. This collaboration could involve sharing resources and expertise to help address the sector’s challenges. The partnership between banks, financial institutions, and the government can negatively affect the economy and the public. Although the collaboration between banks, financial institutions, and the government may have some positive effects, such as increased stability and economic growth, it can also have adverse effects. These negative effects include reduced competition, moral hazard, conflict of interest, undue influence, and financial instability. Therefore, balancing collaboration with effective regulation and oversight is essential to protect the public interest.

In response to the recent SVB banking debacle, the Treasury, Federal Reserve, and FDIC took timely action to mitigate systemic risk. On March 12, they jointly announced that all depositors at both SVB Financial and Signature Bank would be made whole, and a new liquidity facility for depositories was established, with the Bank Term Funding Program offering advances up to the value of pledged collateral. The collateral is valued at par, priced at the one-year overnight index swap rate plus ten basis points (I know I went a bit geeky on that one).

The effectiveness of this action and whether it constitutes a bailout or adheres to Walter Bagehot’s rule for central bankers is subject to interpretation. While equity holders aren’t receiving relief, depositors with uninsured balances are. This type of action has never happened before, and it remains to be seen whether this particular underwriting moral hazard will have long-term costs, but the immediate costs of not doing so would have been dire.

While the recent actions by the Treasury, Federal Reserve, and FDIC may have prevented an immediate banking crisis, it is essential to remember that the underlying issues and challenges facing the banking industry have not disappeared. For example, banks must still navigate challenges such as rising interest rates, increased regulatory scrutiny, and potential liquidity issues. Additionally, investors will likely remain vigilant in scrutinizing banks and may demand increased transparency and accountability.

Furthermore, the recent crisis highlights the importance of risk awareness for consumers and citizens. While most consumers and depositors are protected by FDIC insurance, those with uninsured balances may still be at risk in the event of a banking crisis. Therefore, consumers must be aware of the risks associated with their banking relationships and take steps to minimize their exposure to potential losses. In the case of FDIC insurance, this may mean having multiple accounts at different institutions once your balance reaches over $250,000.

In addition to consumer awareness, it is also essential for policymakers and regulators to remain vigilant in their oversight of the banking industry. While recent government actions may have helped stave off a crisis, it is essential to continue to monitor and regulate the banking industry to prevent future problems. These regulatory actions include ensuring that banks maintain appropriate levels of liquidity, managing systemic risk, and promoting competition and transparency in the industry.

While the recent crisis may have been averted, it serves as a reminder of the ongoing challenges facing the banking industry and the need for continued awareness, regulation, and vigilance. Through continued awareness of these issues, consumers, policymakers, and regulators can help to promote a stable and resilient banking system that serves the needs of all stakeholders.

Conclusion

As the banking industry navigates the challenges and opportunities presented by CBDCs, and the perception of mistrust, it is easy to be both optimistic and skeptical. On the one hand, the potential benefits of CBDCs in terms of efficiency, security, and financial inclusion are significant. On the other hand, the concerns around privacy, regulation, and the role of central banks in the financial system are real and must be clearly and effectively addressed.

To promote a more stable and innovative financial system for the future, it is crucial that all stakeholders, including policymakers, regulators, banks, and consumers, work together. While embracing new technologies, business models, and partnerships can help improve efficiency, enhance customer experience, and mitigate risk, the industry must remain transparent in its approach to innovation.

If the banking industry resists change and fails to address the current crisis of conscience, we risk being left with a stagnant and vulnerable financial system. Therefore, innovation and collaboration must be at the forefront of the banking sector’s response to the industry’s current challenges. Moreover, working together can create a more resilient and trustworthy financial system for all. Hence, innovation, collaboration, transparency, and trust must be at the forefront of the banking sector’s response to its current Crisis of Conscience.